Understanding FinCEN / Anti-Money Laundering Requirements

On March 1, 2026, the data collection and reporting requirements under the U.S. Financial Crimes Enforcement Network (FinCEN) new Anti-Money Laundering (AML) Rule go into effect.

Read our FAQ for more on how this may affect your transaction.

Court Ruling Update – March 19, 2026

On March 19, 2026, the U.S. District Court for the Eastern District of Texas issued a ruling that vacated (set aside) the FinCEN Residential Real Estate Reporting Rule, meaning the court determined the rule could not be enforced at this time.

As a result of this ruling, FinCEN has announced that reporting persons are not currently required to file real estate reports and are not subject to the reporting requirements at this time.

What this means for you:

At this time, we are pausing FinCEN reporting and related information collection while this court ruling is in effect. We will continue to monitor the situation closely and will resume compliance if the rule is reinstated or new federal guidance is issued.

Important Exception — Foreign Entities

Transactions involving foreign-based entities may still be subject to federal reporting requirements under other FinCEN regulations. If your transaction involves a foreign entity, additional information may still be required, and our team will guide you through that process.

What Happens Next?

Because this is a federal matter and is still subject to potential appeal or further rulemaking, requirements may change. Our team is staying up to date on all developments and will guide you through any new requirements if they are reinstated.

If you have questions about how this may affect your transaction, please contact your escrow officer or download our informational flyer regarding this important update.

The Financial Crimes Enforcement Network (FinCEN) is part of the U.S. Treasury Department that enforces anti-money laundering (AML) rules to protect the financial system. In certain cases, the new rules will – by law – require title companies to report certain types of high-value, all-cash purchases to make sure properties aren’t being used to hide illegal money.

For most buyers and sellers, this has little to no impact on the process, but if your transaction falls under FinCEN’s AML rules, you may be asked to provide some additional information or identification. These safeguards help keep the real estate market transparent, secure, and trustworthy for everyone.

When does the rule take effect?

The reporting rule becomes effective on March 1, 2026.

Why did FinCEN create this rule?

Illicit actors often use non-financed (all-cash) residential real estate purchases—especially those involving legal entities or trusts—to avoid scrutiny and hide beneficial ownership. This rule helps law enforcement identify who is behind these transactions and prevents anonymous laundering of illicit funds through real estate.

What types of transactions must be reported?

A transfer is reportable if all of the following apply:

- The property is residential real property located in the United States

- The transfer is non-financed

- The property is transferred to a legal entity or trust

Transfers made directly to an individual are not covered by the AML rule.

What qualifies as residential property?

Residential real property includes:

- Single-family homes

- Townhouses

- Condominiums and cooperatives (including units in large buildings)

- Apartment buildings designed for occupancy by one to four families

- Vacant or unimproved land intended for construction of a one-to-four-family residence.

What is considered a non-financed transfer?

A non-financed transfer is one that does not involve an extension of credit. Specifically, the transaction does not involve funds from an FDIC-insured financial institution, NCUA (credit union) or NAICS (savings bank) member. Non-financed transactions include all-cash, private, individual lenders and seller-carryback loans.

A transfer is reportable when all four conditions are met:

- The real property is residential;

- The transfer is non-financed;

- The property is transferred to certain type of entity or trust; and

- An exception does not apply.

There is no minimum purchase price and gift transfers may also be reportable.

What types of transactions are not reportable?

In most cases, transfers made directly to an individual are not covered by the AML tule.

What is considered a legal entity or trust?

A transferee entity is defined as any person other than a transferee trust or an individual. For example, a transferee entity may be a corporation, partnership, estate, association, or limited liability company. Statutory trusts, which are trusts created or authorized under the Uniform Statutory Trust Entity Act or as enacted by a state, are also considered transferee entities, rather than transferee trusts, for the purposes of this reporting requirement. There are 16 kinds of entities that are exempt from the definition of a transferee entity. A transferee trust is any legal arrangement created when a grantor or settlor places assets under the control of a trustee for the benefit of one or more beneficiaries or for a specified purpose, whether formed under the United States or a foreign jurisdiction. A transferee trust also includes legal arrangements that are similar to such legal arrangements in either structure or function. However, certain types of trusts are exempted from the definition of a transferee trust.

Who is considered a beneficial owner of a transferee entity?

An individual is a beneficial owner if they:

- Exercise substantial control over the entity, or

- Own or control 25% or more of the ownership interests

This definition aligns with FinCEN’s Beneficial Ownership Information (BOI) rule.

Who is considered a beneficial owner of a transferee trust?

Beneficial owners of a trust may include:

- Trustees or individuals with authority over trust assets

- Beneficiaries entitled to all or substantially all trust assets

- Grantors or settlors of revocable trusts

- Beneficial owners of entities or trusts holding these roles

Are there any exemptions from reporting?

Yes. Common exemptions include transfers involving:

- Easements

- Death of an individual (estate, trust, operation of law)

- Divorce or dissolution of marriage or civil union

- Bankruptcy estates

- Court-supervised transfers

- Transfers by an individual (alone or with spouse) to their own trust

- 1031 like-kind exchanges (to a qualified intermediary)

- Transactions where no reporting person is involved

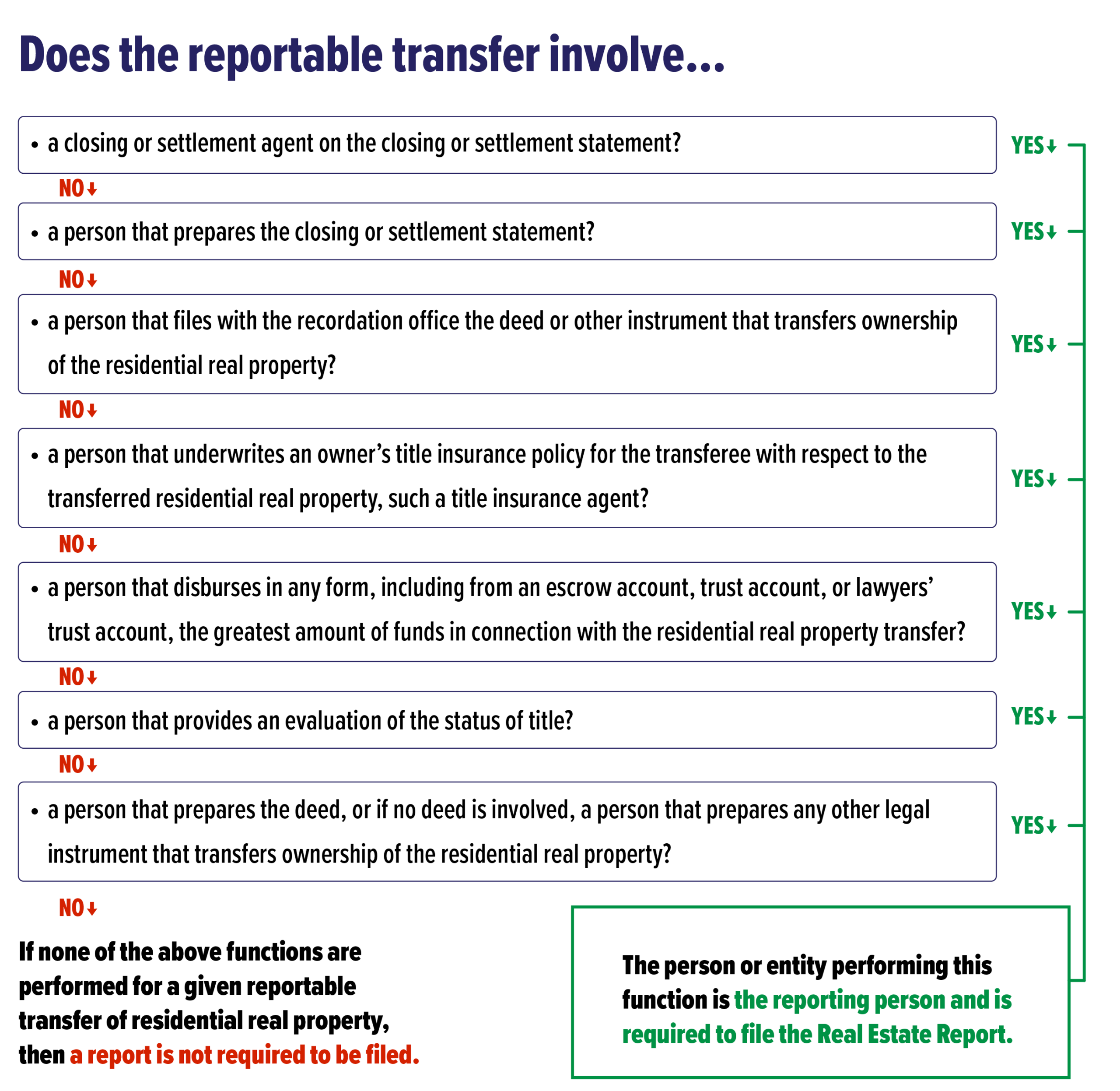

Who is responsible for filing the report?

The person responsible for filing a Real Estate Report is known as the “reporting person,” one of a limited number of persons who play specified roles in the reportable transfer. Only one person in a given transaction is deemed to be the reporting person, and that person is required to report. The reporting person can be identified in one of two ways:

- Reporting Cascade:

- A list of seven different functions that a real estate business or professional may perform in a reportable transfer of residential real property (see below). If a person is performing the first function described in the cascade, then that person would be the reporting person. If no person performing the first function described in the cascade is involved in the transfer, then the reporting person would be the person that performs the second described function, if any, and so on down the cascade.

- If none of the functions set out in the cascade are performed for a given reportable transfer of residential real property, a Real Estate Report is not required to be filed.

- Designation Agreement:

- A person that performs a function described in the reporting cascade may choose to enter into a written agreement that designates another person that performs a function described in the reporting cascade as the reporting person

What information must be reported?

To comply with FinCEN reporting obligations, Pioneer Title Co. may require identifying information for any beneficial owner of a transferee entity or a transferee trust: name, date of birth, residential address, citizenship, and taxpayer identification number. We must report the total consideration paid for the property, along with certain information about any payments made by the transferee entity or transferee trust. Additional documentation or clarification may be requested if required to complete verification or reporting.

When must the report be filed?

The report must be filed by the later of:

- The last day of the month following the month of the transfer, or

- 30 calendar days after closing

Failure to comply with reporting obligations can result in civil and criminal penalties under the federal Bank Secrecy Act (BSA).

How is the report filed?

Pioneer Title utilizes Real Estate Report, a third-party reporting service from Advalis, Inc. Due to the increased time, verification, documentation, and reporting required to comply with FinCEN AML regulations, an additional compliance fee of $200.00 will apply to transactions subject to these reporting requirements. This fee, imposed by all title companies, reflects the administrative regulatory burden associated with federal compliance and will be disclosed on your settlement statement.

Are records required to be kept?

Yes. While a copy of the report itself does not need to be retained, reporting persons must keep for five years:

- Certifications of beneficial ownership information

- Written designation agreements (if applicable)

Is reportable identifying information kept secure?

Yes. All information collected for AML compliance is handled in accordance with applicable privacy laws and is used exclusively for regulatory reporting purposes. Pioneer Title Co. does not use this information for marketing or any non-compliance-related purpose.

Why This Matters

The Financial Crimes Enforcement Network (FinCEN) Anti-Money Laundering (AML) rule is part of a broader federal effort to promote transparency in real estate transactions and prevent the use of property purchases for illicit activity. While these requirements may feel new or unfamiliar, they are becoming a permanent and expanding part of the real estate landscape nationwide.

At Pioneer Title Company, compliance with federal regulations is not optional—it’s a responsibility we take seriously. Our role is to guide transactions forward while ensuring all reporting, verification, and documentation requirements are met accurately and securely.

What This Means for You

- Some transactions require additional information and verification

- Requests for personal or entity details are driven by federal law—not company policy

- Additional time and a compliance fee may be required for transactions subject to AML reporting

Our Commitment

We are committed to:

• Protecting your privacy and handling information responsibly

• Communicating requirements clearly and early in the process

• Minimizing delays while meeting all legal obligations

If your transaction falls under FinCEN AML reporting requirements, your Pioneer Title Company escrow officer will walk you through each step and explain what is needed and why. Our goal is to keep your transaction moving smoothly—while doing our part to uphold the integrity of the real estate industry.

If you have additional questions, we encourage you to reach out to your escrow officer. We’re here to help.